When dealing with financial transactions between related parties, particularly in the case of intercompany loans, a key issue is determining the appropriate interest rate to apply. Naturally, this interest rate is tied to the default risk level of the borrowing entity, which is typically measured through a credit rating.

However, it is common to encounter situations where the specific borrowing entity lacks an individual credit rating, while the multinational group to which it belongs does have one. In such cases, the OECD Transfer Pricing Guidelines allow for approximating credit risk using the credit rating of the multinational group (paragraph 1.171). Nevertheless, the Guidelines also caution that these methods may lack sufficient robustness, and therefore it may be advisable to consider the group’s credit rating.

Thus, it is relevant to examine some of the implications of using this approach. To do so, we will revisit a few concepts from credit portfolio theory to highlight certain key points:

The n – th return on a portfolio of assets is defined as follows:

Where:

= El porcentaje del i – th activo que compone la cartera.

= El porcentaje del i – th activo que compone la cartera. = El rendimiento del i – th activo que compone la cartera.

= El rendimiento del i – th activo que compone la cartera.

Two important measures for analyzing portfolio risk are the expected value (mean) and the variance. These reflect both the anticipated return and the volatility of the portfolio, respectively.

The expected return of the portfolio is calculated as:

Where:

= The n – th observation of the return of the i – th activo que compone la cartera.

= The n – th observation of the return of the i – th activo que compone la cartera.- N = Number of observations

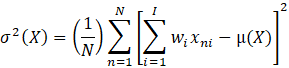

The variance of the population is given by:

Such that.

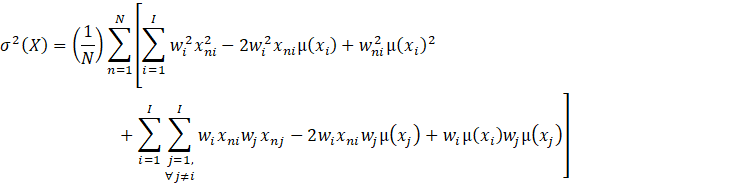

Expanding the definition, we find:

Given that.

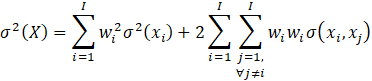

We obtain.

Where:

= denotes the covariance between the i – th and j – th a assets in the portfolio,

= denotes the covariance between the i – th and j – th a assets in the portfolio,  .

.

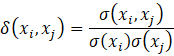

By expressing the variance equation in terms of the correlation coefficient, defined as:

we obtain the following expression:

Taking the partial derivative of ![]() with respect to

with respect to ![]() we obtain:

we obtain:

Alternatively, assuming perfect correlation between all assets, that is, ![]() , we obtain:

, we obtain:

From equation (a), it follows that the risk of the portfolio decreases as the correlation between assets decreases, due to the benefits of risk diversification. On the other hand, equation (b) shows that in the case of perfect correlation between all assets in a portfolio, the standard deviation of the portfolio is equal to the weighted average of the standard deviations of the individual assets.

Therefore, we can conclude that unless there is perfect correlation among all assets in a portfolio, the portfolio risk will be lower than the weighted average of the individual asset risks.

In the case of a multinational group, it can be viewed analogously to a portfolio, where the entities comprising the group are equivalent to the individual assets, and the group’s credit rating corresponds to the risk of the portfolio representing the group.

However, in favor of applying the arm’s length principle, the benefits of risk diversification should not be taken into account, since these benefits are only meaningful from the perspective of the group’s shareholders and only materialize due to the related-party nature of the entities. Therefore, such a benefit should not be recognized under the arm’s length principle.

As a result, a multinational group credit rating that is aligned with the arm’s length principle would be equivalent to the rating that would result under the assumption of perfect correlation among all group entities. Otherwise, we would be using a credit rating that reflects a lower level of risk.

Given that it is quite reasonable to assume that a perfect correlation does not exist in a real-world multinational group, the conclusion is that relying on the group’s consolidated credit rating would lead to a systematic underestimation of its actual credit risk.